Changed audit expectation gap for audit services in the digital age

by Aldo Dubacher

What are the effects of the digital transformation of companies in the age of big data on the authenticity of audit evidence and data analysis techniques? Does this result in a new audit expectation gap?

Digitization increases the transaction volume

Digital transformation creates new business models. The high level of innovation in the FinTech industry in Switzerland is revolutionising banking services in the Swiss financial market, for example. New types of ERP systems book transactions in a more complex way to expand data analysis options. The automation of accounting processes combined with a new business model is leading to a sharp increase in transaction volume. Due to the nature of the system, audit evidence is only processed electronically and presented digitally to the auditor.

Authenticity of audit evidence as a challenge

This creates new challenges for auditors when assessing the authenticity of audit evidence. The International Standard on Auditing 500 - Audit Evidence (ISA 500) was last updated in 2009 and dates back to an era when digital transformation was only in its beginning.

ISA 500 clause 7 requires an auditor to consider the relevance and reliability of information used as audit evidence. Digital signatures in electronic documents can increase the authenticity of the audit evidence and protect documents from manipulation. However, from my own experience, “reading” such digital signatures is not always easy. In addition, digital signatures cannot be integrated into all electronic audit records.

The critical auditor would do well to obtain third-party confirmations from counterparties for audit clients with increased audit risks, and for significant balance sheet items if there are doubts about the authenticity of the audit evidence.

Changing the focus of data analysis in the Big Data environment

Data analysis techniques have been used by auditors for some time. In the early days, the procurement of data from audit customers often represented a difficult hurdle, which was very time consuming, resulting in data analysis techniques that were not efficient enough.

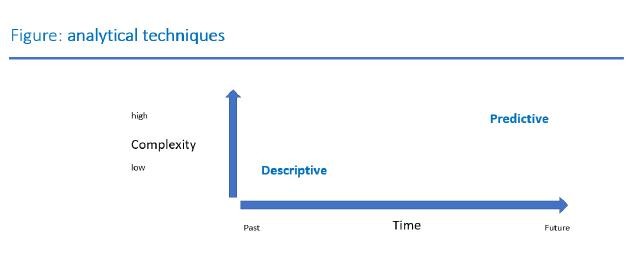

The focus of 20th century data analysis was descriptive (what happened), and had a "diagnostic" background as to why certain transactions happened (past-oriented). Since the age of Big Data began, the focus of data analysis has shifted to predictive (what will happen) in order to predict developments; it is therefore much more future-oriented.

Exemplified by large-scale data lake projects in companies in industries such as retail or banking, a system or repository of data is stored in raw data format. A data lake is typically a single repository for all enterprise data, including raw copies of source system data. Data lake projects are in the process of replacing former data warehouse solutions.

The progress made in synchronising and merging relational databases led to the standardisation of database structures, which simplified access for auditors to general ledger and subledger data of audit clients. However, the greatest challenge remains in assessing the underlying data quality, which the auditor must critically do before the analyses are prepared.

Expanding the audit expectation gap?

In teaching, the classic audit expectation gap is understood to mean that the target groups of audit reports sometimes have very different expectations regarding the work of the auditor. They often assume that an unmodified audit report, beyond the audit statements, means, for example, that the auditor has verified that the company is complying with all relevant laws and thus errors in the annual financial statements can be ruled out with absolute certainty. Such expectations, however, go beyond the tasks of the auditor as they result from the legal provisions and the regulations of the profession (the so-called “expectation gap”).

With the proliferation of data analytics, audit clients and their stakeholders are presented with the idea that sample- based auditing will be overcome through the use of all-encompassing data analytics (including vouchers). Thanks to digitisation, the auditor has easier access to the entire general ledger and subledger data. An examination on a sample basis is no longer necessary.

This widens the audit expectation gap, assuming that the audit covers the entire data universe of the audited company. However, the core performance of data analysis remains in interpreting the analysed data, which business intelligence can currently only support but not replace. The auditor's interpretation of the results of the data analysis must also continue to be based on random samples.

Impact on the relationship with the audit client

The auditing profession should explain this audit expectation gap and communicate openly with audit clients and stakeholders.

Data analysis should not only generate additional audit evidence for us as auditors, but also create additional benefits for CFOs of the audited companies.

This way, audit clients will understand full data immersion and will make better business decisions themselves. The quality of decision-making will shift by itself from “descriptive” to “predictive”.

Photo: lena_serditova - stock.adobe.com

/https://storage.googleapis.com/ggi-backend-prod/public/media/3674/zurich-a227941134.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/6031/FINAL-IFRS-shutterstock_2195144437-(1)-cropped.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/6030/FINAL-ESG-shutterstock_1919560145-cropped.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/6029/ARC_Alok-Kumar-cropped.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/6028/FINAL-whistleblower-law-shutterstock_1022819620-(1)-cropped.jpg)