Sustainability - a new frontier for Italian companies

Nowadays in Italy, if we open the pages of a newspaper, listen to the news, or engage with businesses, banks, or local administrators, we cannot fail to notice that sustainability is at the heart of the debate.

Sustainable development – the guiding principle of sustainability – is aimed at meeting the needs of the present generation without compromising the ability of future generations to meet their own.

The combined effect of the post-pandemic landscape and the Russian-Ukrainian war has accelerated the shift from a shareholder-oriented to a stakeholder-oriented business concept which is the base for the sustainability development.

Today the benefits associated with corporate social responsibility (CSR) are, among others: increased access to credit, the reduced cost of money, the ability to provide relevant information to potential and actual investors, and savings in production operating costs.

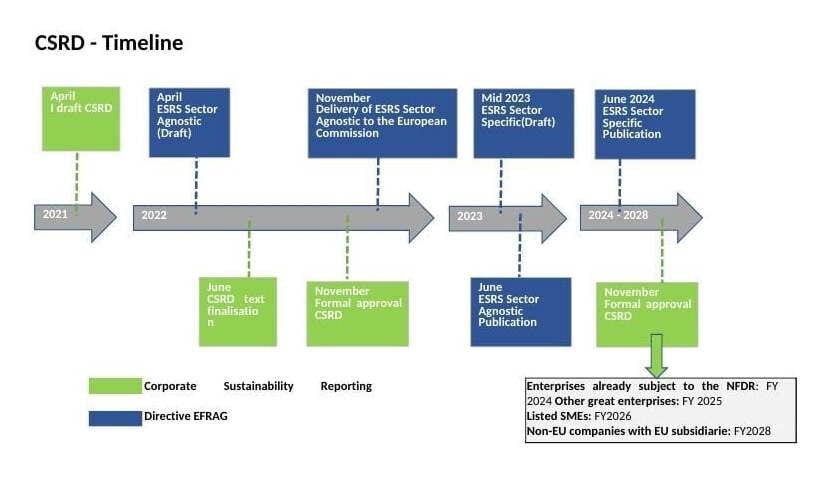

The Corporate Sustainability Reporting Directive (CSRD) broadens the spectrum of European companies obliged to communicate sustainability from about 10,000 to 50,000 companies, but the directive’s orientation is to make these sustainability regulations also applicable to additional smaller and mid-sized companies. This is both because SMEs are part of the production chain of large companies and because they too have a significant impact on the community.

To do this, the European Financial Reporting Advisory Group (EFRAG) was commissioned to draw up mandatory European standards. In addition, double materiality provides the information needed to understand the company's impact on sustainability issues (inside-out perspective), as well as how these issues affect the company's development, performance and positioning (an outside-in perspective). Of course, ESG issues are the subject of reporting and the information should be qualitative and quantitative, prospective and retrospective, and cover short, medium, and long-term time horizons.

By improving the quality, availability and comparability of information, European sustainability reporting standards (ESRS) have the potential to reduce costs for all stakeholders, but the real impact cannot yet be determined. There will also be indirect benefits related to the need for changes in companies' organisational models and a substantial improvement in sustainability levels.

Finally, not to be underestimated is the aspect of an assurance of the quality of the sustainability reporting. Asseveration increases the credibility of the disclosure and the confidence of investors; it contributes to strengthening positive market effects and is an important element that enhances the credibility of sustainability communication.

For Italian and European companies in general, beyond legal obligations, it is of fundamental importance to start considering the effects of sustainability reports. These include the fact that as ESG performance increases, future cash flows (FCF) increase, the weighted average cost (WACC) decreases, and the final value of the company tends to grow.

/https://storage.googleapis.com/ggi-backend-prod/public/media/4874/FINAL-ESG-shutterstock_2242996813-square-small.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/1833/imagecCOFjn.png)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7111/7a52428d-5e91-45c9-8d88-9802f4dc2297.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7110/3455a5d5-2ba4-47a4-b6c0-bf8cf9fbef02.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7109/40f50fe9-a9e3-44f2-8401-9874c36feb9f.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7108/4a95da83-6b25-41b7-99a1-5c891da90b5f.jpg)