Transfer pricing in Singapore

by Eddie Lee

1. Introduction

Transfer Pricing (“TP”) is an essential aspect of the regulatory requirements in Singapore for companies which have intra-group transactions or related party transactions (“RPTs”) in Singapore and if they expand their businesses outside Singapore. TP rules require that those RPTs are conducted at arm's length prices, which refers to prices that would be agreed upon by unrelated parties in similar situations.

2. Transfer Pricing Regulations and Practices

Please note that there are two major compliance requirements under the Income Tax Act.

a. Section 34D – Arm’s Length Principles

- Under Section 34D, all Singapore businesses are required to adhere to the arms’ length basis of pricing for its RPTs except for certain transactions for which exemptions apply. The exemptions are summarized separately under Exemption from TPD Preparation (page 4). This RPTs can be the purchase of goods, provision of services, borrowing or lending of money, use or transfer of intangibles and etc where the pricing should reflect the arm’s length principle.

- In relation to the above, the arm’s length principle is the international standard to guide the transfer pricing between related parties. All companies in Singapore which have RPTs must adopt the arm’s length principle by charging the related party same as the third party.

- It is pertinent to add that IRAS subscribes to the principles that profits should be taxed where the real economic activities generating the profits are performed and where value is created. A proper application of the transfer pricing rules would ensure this outcome.

- Where the pricing of the RPTs is not on arm’s length basis, IRAS may adjust the profit and tax liability of the errant taxpayer.

- Apart from TP adjustments, a 5% surcharge may be levied on any additional tax liabilities resulting from such TP adjustments. Last but not least, IRAS may also impose penalties of up to 200% on the undercharged tax payable.

- Where a company’s total value of RPTs (including loans) exceeds $15 million in a year, it is required to disclose the details of its RPT to Inland Revenue Authority of Singapore (“IRAS”) in its annual tax return. These details of RPT include the nature of transactions, identities, and their specific relationship. In most cases, this information will serve as a risk management tool for IRAS to assess transfer pricing risk and compliance.

b. Section 34F – Transfer Pricing Documentations

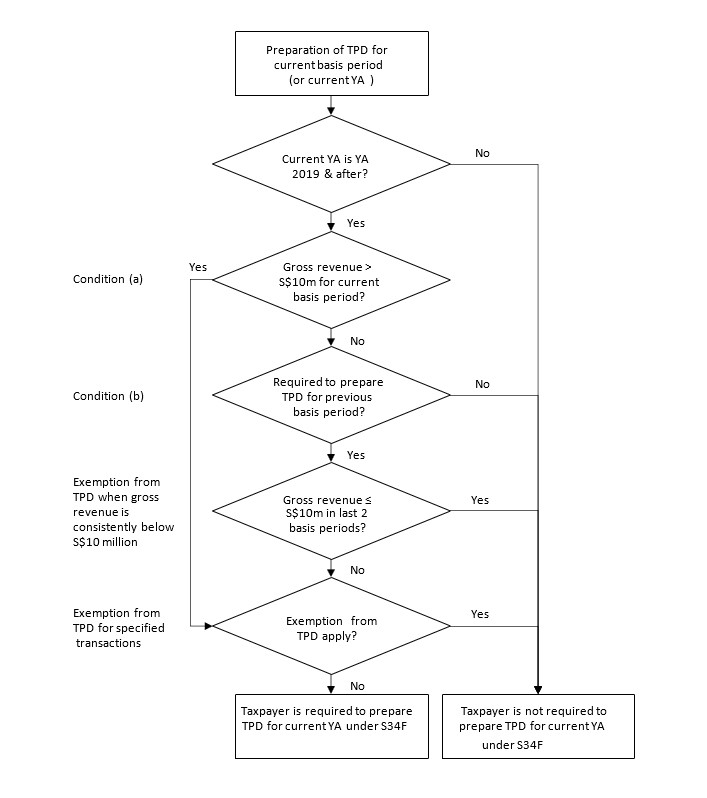

- Under Section 34F, all Singapore businesses have to prepare a contemporaneous (i.e. requiring real-time data) Transfer Pricing Documentation (“TPD”) for submission to IRAS if their annual revenue/turnover is more than $10 million and they did not meet the annual exemption threshold for the specific RPTs.

- The TPD is a report to substantiate that all RPTs within a group of companies are finalised on arm’s length basis, meaning that the prices or margins of these intercompany transactions are comparable to what would have been entered into between outside or unrelated parties.

- As long as the details in the TPD remain accurate, it should be refreshed once every three years.

- The TPD must be kept for at least 5 years from the end of the basis period in which the RPT took place.

Summary of major requirements for preparing TPD under Section 34F

| Scope | TPD requirements |

| When it takes effect | From YA 2019 |

| Who must prepare |

Companies who meet either of the following conditions must prepare TPD for their related party transactions undertaken in a basis period:

|

| What to prepare | The details are prescribed in the TPD Rules and in IRAS tax guidelines. |

| When to prepare | Not later than the filing due date of the tax return. |

| When to submit | Within 30 days from date of request by IRAS to submit the TPD to IRAS. |

| How long to retain TPD | At least 5 years from the end of the basis period in which the RPTs took place. |

| When to refresh TPD | When to refresh TPD As long as the details in the TPD remain accurate, Companies may refresh their TPD once every three years. |

| Scope | TP documentation requirement |

| Contemporaneous basis | Should be prepared on a contemporaneous basis. (i.e. information existing at the time of the RPTs) |

| Exemption from preparing | The exemptions from preparing TPD (see summary below) |

| Penalty for non compliance | A fine not exceeding $10,000 |

c. Exemption from TPD Preparation

In situations where the gross annual revenue from trade or business is consistently below $10 million, exemption from TPD is applicable. It is also applicable where the gross annual revenue from trade or business is NOT more than $10 million for the period but where TPD was mandatory in the immediate two preceding basis periods.

| List of Specific Transactions Qualifying for TPD Exemption | Value per annum (S$) |

| 1. Related party domestic transactions subject to the same Singapore tax rate | No limit |

| 2. Related party domestic loan | No limit |

| 3. Related party loan with indicative margin applied above base loan interest rates | Loan below 15 million |

| 4. Routine support services on which a 5% cost plus is applied | No limit |

| 5. Related party transactions covered by an Advance Pricing Agreement with IRAS | No limit |

| 6. Purchase of goods from a related party (amount paid or payable) | Below 15 million |

| 7. Sale of goods to a related party (gross revenue from sale) | Below 15 million |

| 8. Loan by a related party (Principal amount of loan) | Below 15 million |

| 9. Loan to a related party (Principal amount of loan) | Below 15 million |

| 10. Provision of services to a related party (amount of fees received or receivable) | Below 1 million |

| 11. Provision of services from a related party (amount of fees paid or payable) | Below 1 million |

| 12. Royalties or license fees from a related party (amount of fees received or receivable) | Below 1 million |

| 13. Royalties or license fees to a related party (amount of fees paid or payable) | Below 1 million |

| 14. Lease or rental received from a related party (amount received or receivable) | Below 1 million |

| 15. Lease or rental payable to a related party (amount received or receivable) | Below 1 million |

| 16. Any other related party transaction not covered by the above | Below 1 million |

3. An Illustration of TPD Requirements

Source: www.iras.gov.sg

4. IRAS Tax Guidelines

The primary objective of the IRAS guidelines serves to provide companies with an understanding of the TP laws and regulations which cover the following areas:

- Application of the arm’s length principle when transacting with their related parties,

- Application of the arm’s length principle for specific RPTs such as related party services and loans,

- Preparation and maintenance of contemporaneous TPD for submission to IRAS,

- Procedure and process for avoidance and resolution of TP disputes under the double taxation agreements (“DTA”) between Singapore and treaty countries,

- Clarification on the various implications of non-compliance with transfer pricing requirements, and

- Overview of transfer pricing compliance programme and IRAS position regarding various transfer pricing matters.

5. The Three-Steps Approach

IRAS recommends that taxpayers adopt the Transfer Pricing Analysis which is the 3-step approach to apply the arm’s length principle in their related party transactions:

a. Step 1 – Comparability Analysis

It is necessary to conduct a comparative study of the relevant RPT by applying the arm’s length principle. Essentially this step involves identifying comparable situations or transactions between independent parties against which the RPTs and profit margin is to be benchmarked. This is commonly known as “comparability analysis”. The testing of this comparability analysis will become a comprehensive assessment and identification of significant similarities and differences (i.e. products, characteristics, functions performed and etc) between the related party transaction with those in an independent party transaction. In case of any reasonable adjustments to be made for material differences, the method of computation should be documented.

The comparability for every RPTs should cover the following aspects:

- Terms of contract (i.e credit or cash terms),

- Characteristics of goods, services, or intangible properties,

- Details of functions performed (i.e. delivery, promotional & advertising),

- Assets in use and risks undertaken (“FAR”), and

- Commercial and economic situations (i.e. The business environment).

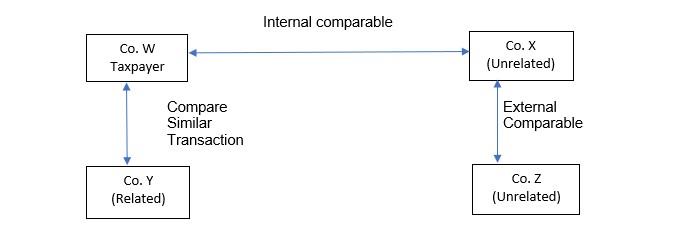

An illustration of a comparative analysis is shown below.

(i) Internal comparable

Price or margin in a comparable transaction between one party which is a party to the related party transaction and an independent party. (i.e. Co. X & Co. Y)

(ii) External comparable

Price or margin in a comparable transaction between two independent parties, neither of which is a party to the related party transaction. (i.e. Co Z & Co. X)

b. Step 2 – Choice of Transfer Pricing Methods

IRAS recommendation involved identifying the appropriate transfer pricing method. There are five internationally accepted methods for evaluating a taxpayer’s transfer pricing or margin against a benchmark based on the prices or margins adopted by independent parties in similar transactions. These are discussed separately under the “Transfer Pricing Methods”

| Methods | Category |

| 1. Comparable Uncontrolled Price (“CUP”) method | Traditional Transaction Methods |

| 2. Resale Price (“RP”) method | Traditional Transaction Methods |

| 3. Cost-Plus (“CP”) method | Traditional Transaction Methods |

| 4. Transactional Profit split (“PS”) method | Transactional Profits Methods |

| 5. Transactional Net Margin method (TNMM) | Transactional Profits Methods |

c. Step 3 – Testing the Arm’s Length Results

After step 2 has been completed and an appropriate TP method has been identified, it is then tested to the data of a comparable independent party transaction to arrive at the arm’s length result. To enhance the reliability of the comparability analysis, taxpayers could apply the interquartile range to determine the arm’s length remuneration. IRAS will accept the use of a range of prices or margins (i.e. interquartile range) resulting from the transfer pricing analysis provided the comparable are reliable.

It is recommended that the RPTs are tested periodically against arm’s length results acquired annually and appropriate year-end adjustments are made at the end of each financial year.

6. Transfer Pricing Methods

a. Comparable Uncontrolled Price (“CUP”) Method

- This method compares the price charged in a RPT to the price charged in an independent transaction in comparable circumstances.

- It is reliable if there is a high level of comparability between the related party transaction and the independent party transaction.

- It is the most direct way to determine arm’s length price as compared with other TP methods. However, a less direct method is necessary if comparable independent-party transactions cannot be found.

- This method is preferred for transactions involving products with similar characteristics (type, physical features, quality, quantity) and in a similar market or economic situations (e.g. widely traded commodities).

b. Resale Price (“RP”) Method

- The RP method is preferred where a product that has been purchased from a related party and then resold to a third-party customer. The RP to the customer is reduced by a gross margin (the “RP margin”) to arrive at the arm’s length price of the RPT between the related parties.

- Under arm’s length conditions, the RP margin should allow the reseller to recover its selling and other operating costs, and earn a reasonable profit based on the functions performed, assets used, and risks assumed.

- The RP method is most appropriate where the reseller adds relatively little value to the properties prior to selling to third-party customers.

c. Cost-Plus (“CP”) Method

- The CP method uses the gross markup obtained by a supplier for the property transferred or services provided to a related purchaser. Essentially, it values the functions performed by the supplier of the property or services. As a result, a comparable gross markup is added to the costs of the supplier of goods or services (“cost base”) in the RPT to arrive at the arm’s length price of that transaction.

- Both the CP and RP methods are similar to the extent that fewer adjustments are required to account for product differences, as compared to CUP method. Other factors of comparability, such as the FAR and economic circumstances of the tested party, are more appropriate to apply in the CP method.

- Applying the CP method requires the comparability of the gross markup and cost base in the related and independent party transactions. If the related and independent party transactions are not comparable in all aspects and the differences have a material effect on the price or margin, adjustments should be made to eliminate the effects of those differences.

- In applying this method, the cost base can be categorised as follows:

Type of cost Examples Direct costs • Cost of raw materials

• Cost of labourIndirect costs • Depreciation

• Repair and maintenance which may be allocated among several productsOperating expenses • Marketing

• General and administrative

Source: www.iras.gov.sg

- In this method, a comparable gross markup is added to the costs of the supplier of goods or services (“cost base”) in the related party transaction to arrive at the arm’s length price of that transaction.

- Generally, costs can be categorised as direct costs, indirect costs, and operating expenses. In applying the cost-plus method, direct and indirect costs of producing a good or providing a service are normally used to compute the cost base. Such costs are limited to the costs of the supplier of goods or services and should take into account an analysis of the supplier’s FAR.

- The CP method is most useful where semi-finished goods are sold between related parties or where the related party transaction involves the provision of services.

d. Transactional Profit Split (“PS”) Method

- The transactional profit split method is based on the concept of splitting the combined profits of a transaction equitable between related parties in a similar way as how independent parties would under comparable circumstances.

- Briefly, the profits are to be split is the operating profit, although occasionally, it may be appropriate to carry out a spilt of gross profit and then deduct the expenses incurred by or attributed to each relevant party.

- It is particularly useful in the following situations where:

i. RPTs are highly interrelated that they cannot be evaluated separately.

ii. Each related party makes unique and valuable contributions to the transaction.

iii. The existence of unique intangible assets makes it difficult to find reliable comparable. - Generally, there are two approaches to apply the Transactional PS Method:

i. Residual analysis approach

This is preferred and it involves two stages:

Stage 1 - Determine the return for routine contributions

Stage 2 - Divide the residual profit

ii. Contribution analysis approach

This approach uses the total profit earned by both parties in the RPT to divide against their relative contributions to earning that profit. This calculation should be supported by comparable data, if available.

e. Transactional Net Margin Method (“TNMM”)

- The TNMM compares the net profit relative to an appropriate base such as costs, sales, or assets that is attained from a RPT to that of comparable independent parties. By using this method, a price would be considered charged at arm’s length if the net profit margin is comparable to functions, bearing similar risks and employing similar assets.

- TNMM method is similar to the RP and CP methods. The main difference between the TNMM and both methods is that the former is more focused on the net margin instead of the gross margin of a transaction.

7. IRAS Specific Guidance

IRAS provides specific guidance on certain RPT services such as the followings.

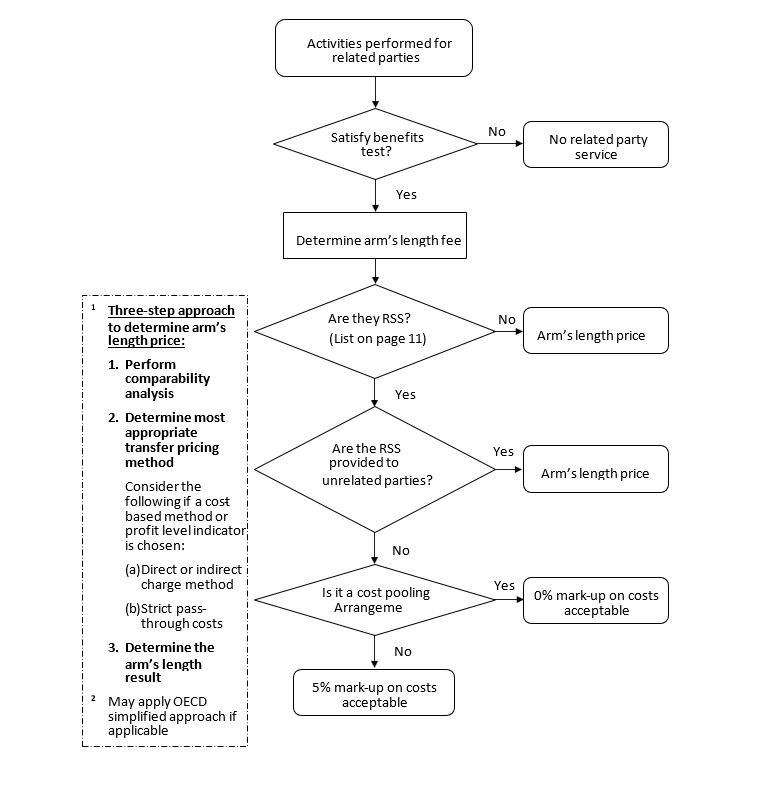

a. Provision of related party services

- There should be an arm’s length charge for provision of services provided between related parties, which is comparable to the cost of similar services between two or more unrelated parties under similar circumstances.

- Generally, the performance of activities for the related party should be subject to a “benefit test”. This is to verify whether the recipient of the services receives, or reasonably expects to receive any benefit from such activities. Likewise, is there any commercial or economic benefit such that an independent party would expect to pay to receive the benefits or be paid for providing the benefits.

b. Strict Pass-Through Costs

- • These are expenses that are charged without any markup and are usually payments made on behalf of the related party.

- • In a RPT between two related parties (say, A & B) the supplier of the services (A) may acquire these supplies from another service provider (third party) and make payment on behalf the other related party (B). The related party (B) will have to bear the costs of the third-party supplier as (A) pays on behalf of related party (B). When the (A) pays to the third party, IRAS is prepared to treat these as strict pass-through costs and accept no markup on the charges when the following conditions are met:

i. Services are acquired for the benefit of the related parties,

ii. Services are acquired and have been charged at an arm’s length,

iii. Only payment is made and does not enhance the value of acquired services,

iv. Costs incurred on behalf of the other related parties.

c. Routine Support Services (RSS)

- IRAS has clarified that it will impose a 5% markup on the provision of RSS between related party. A list of RSS is also provided by IRAS as given below.

Nature of Routine Support Services Qualifying conditions Accounting and auditing Must be routine support services (RSS). Account receivable and payables Must be routine support services (RSS). Budgeting Must be routine support services (RSS). Computer support Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Database administration Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) General administrative Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Legal services Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Payroll Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Corporate services Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Payroll Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Corporate communication Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Staffing & Recruitment Must not provide the same routine support services to an unrelated party. (e.g. accounting firm provides accounting services to related party => failed the condition) Tax All costs including direct costs, indirect costs, and operating costs relating to RSS. Training and employee development All costs including direct costs, indirect costs, and operating costs relating to RSS. Management reporting All costs including direct costs, indirect costs, and operating costs relating to RSS.

Source: www.iras.gov.sg

d. Markup Price Other Than 5%

For a markup that is different from the recommended 5% basis, the services providers should be able to:

- Support their basis with a detailed transfer pricing analysis,

- Apply the markup consistently except where there are material changes to the circumstances or services provided, and

- Review the rate of markup regularly to ensure that it continues to reflect arm’s length conditions in their situations.

e. Cost Pooling Arrangement (there is no markup in the cost pooling)

In a cost pooling arrangement between members of a corporate group in common need of RSS, they may share the costs of such services subject to the following conditions:

- Each of the member is reasonably expected to benefit or actually benefit from the services in respect of which costs are being shared, and

- They contribute on arm’s length basis, to the costs of providing the service in proportion to the nature and extent of expected benefits that it receives.

Under IRAS administrative concession, any payments for RSS under the cost-pooling arrangement may be charged without markup subject to the following conditions:

- Costs must be shared by each of the members in the form of cash or other monetary contributions,

- The RSS are not provided to any unrelated party,

- The provision of the RSS to the related parties is not the main principle activity of the service provider,

- Sufficient documentation to support the contracting parties intended to enter into a cost-pooling arrangement prior to the provision of the RSS. Such documents should contain the description of the nature of services, reason for selection of a specific method of allocating costs, calculation and share of contributions by each member and any anticipated benefits thereof.

f. Related Party Loans

A loan can be in any form regardless of whether or not it is made through a written agreement and it includes:

- Credit facilities, or

- Intercompany credit balance arising from the normal course of sales and provision of services that are left uncollected over a substantial period of time which a third-party creditor would typically allow.

There are generally two types of related party loans identified by IRAS, namely,

- Related Domestic Loan (“RDL”)

When a Singapore entity lends money to or borrows money from another related Singapore entity, this is referring to as a RDL. In simple terms, borrowers and lenders are both in Singapore and are Singapore entities. In this case, the lender is required to adopt an interest restriction method on its claim for external financing costs. - Related Cross Border Loans (“RCBL”)

Where a Singapore entity lends money to or borrows money from another related foreign entity (outside Singapore) this is referring to as a RCBL. In simple terms, either the borrowers or lenders is in Singapore and outside Singapore entities. In this situation, the related companies in Singapore should adopt the 3-steps approach to calculate the arm’s length interest charged. As an IRAS administrative concession, companies may choose to apply an indicative margin which will be published and updated at the beginning of each year to an appropriate base reference rate for all related party loans provided that the related party loans do not exceed $15 million at the loan is obtained or provided.

Up to 2021, the indicative margin are applicable to Interbank Offered rates (IBOR) as base reference rates such as Singapore Inter Bank Offered rates (SIBOR) and the London Inter Bank Offered rates (LIBOR). However, with effect in 2022, with the decommissioning of LIBOR, IRAS has enhanced the methodology to derive indicative margins through the transit of IBORs to Risk-Free rates (RFRs) as the base reference rates such as Singapore Overnight Rate Average (SORA), Secured Overnight Financing Rate (SOFR), Sterling Overnight Index Average (SONIA).

o Indicative margin** + Singapore Overnight Rate Average (SORA)

o Indicative margin** + Secured Overnight Financing Rate (SOFR)

o Indicative margin** + Sterling Overnight Index Average (SONIA)

**In the year 2022, the indicative margin for related party loan not exceeding $15 million obtained or provided is 1.80%.

g. OECD 5% Markup

Where intra-group services do not fall within “RSS”, companies may apply the OECD simplified approach where a 5% cost mark-up is used to charge the related party for the services rendered subject to the following conditions:

- These are low value-added services which are supportive in nature and not part of a core-business of the group.

- The RSS is not specifically excluded as intra-group services under the OECD simplified approach.

- The tax authorities in this RSS transactions must similarly adopted the OECD simplified approach.

- The same RSS should not be offered to any unrelated party, and

- All costs relating to RSS must be included (direct, indirect and operating costs).

8. An illustration of Application of Arm’s Length Principle in RPT Services

Source: www.iras.gov.sg

9. Organization for Economic Co-operation and Development (“OECD”)

OECD also issued the transfer pricing guidelines for Multinational Enterprise and Tax Administrations in 1995 and provides guidance on the application of the “arm's length principle”, as the international consensus to help transactions between related parties, to be priced appropriately and that profits are allocated fairly. i.e. on the valuation for tax purposes of cross-border transactions between associated enterprises.

The OECD Guidelines also provide guidance on the principles and methods for determining transfer prices for related-party transactions, and include the three steps approach, earlier discussed by us, on TPD.

IRAS also adopts the TP methods (see page 8) which describe several TP methods, including the CUP, RP, CP, and the PS methods. These methods are used to determine arm's length prices for RPTs based on the prices that would be charged in comparable transactions between unrelated parties.

It is important for multinational enterprises to follow the OECD transfer pricing guidelines to ensure compliance with tax laws and to avoid disputes with tax authorities in different countries. By following these guidelines, enterprises can help ensure that their transfer pricing policies are transparent, consistent, and supportable.

Singapore similarly adopts the guidelines provided by OECD.

10. Economic and Analysis to Determine Arm’s Length Result

Economic analysis is an important aspect of TPD in Singapore. In which economically significant activities and responsibilities undertaken, assets used, contributed, and risks assumed (“FAR”) by the parties to the transactions are identified and subject to comparative analysis. The results are meant to demonstrate the arm's length basis o RPTs in Singapore. In the economic analysis, various application of economic principles and methodologies are involved to determine the RPTs at arm's length.

This analysis typically involves the following steps:

- Selection of the transfer pricing method:

The first step in the economic analysis is to select the most appropriate TP method for the relevant RPT. As discussed earlier, the IRAS recognizes 5 TP methods - Selection of comparable data:

The second step is to identify the relevant comparable data, with similarity in terms of product, service, or function. - Application of the transfer pricing method:

The process in step 1 and 2 are then applied to determine the arm's length price of the transaction. - Documentation of the economic analysis:

The last step refers to the documentation of the economic analysis to demonstrate how the arm's length principle has been met.

11. Advanced Pricing Agreements (APAs), Dispute Avoidance and Resolution

APAs are agreements made in advance with IRAS and foreign tax authorities regarding the pricing of a RPT upon taxpayer’s application relating to a specific time-period. Upon successful application, IRAS may grant exemption for the preparation of the TPD where the RPTs are covered by the APA. The successful applicant must keep relevant documents for the purpose of preparing the annual compliance report to demonstrate compliance with the terms the APA, with essential assumptions unchanged.

APAs can be uni-lateral, bi-lateral of multi-lateral agreements made between IRAS and:

- The taxpayer (uni-lateral),

- A tax treaty member on TP of RPTs between entities of both territories (bi-lateral),

- Two or more tax treaty members on the TP of RPTs between entities in these territories (multi-lateral).

Suffice is to add that the level of certainty in a uni-lateral APA is lower by comparison to that of one under the bi-lateral or multi-lateral APA. The reason is that the terms of the APA are non-binding in the case of a foreign tax authority which is not a party to the APA.

If Singapore does not have a DTA with the other tax jurisdictions, the unilateral APA comes under the framework of Singapore's Advance Ruling System and a fee will be charged. If Singapore has a DTA with the other jurisdiction, the unilateral APA will be issued outside of the Advance Ruling System, and there is no fee will be charged for the unilateral APA from IRAS.

The Final Report on Action 5 “Countering Harmful Tax Practices More Effectively, taking into Account Transparency and Substance” published by the OECD in October 2015 forms a basis of an agreed framework for the compulsory spontaneous exchange of information in respect of rulings. In essence, IRAS is obligated to have spontaneously exchange information on cross-border transactions under the uni-lateral APAs with certain jurisdictions.

Photo: jasckal - stock.adobe.com

/https://storage.googleapis.com/ggi-backend-prod/public/media/3255/singapore-a179604362.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3265/turin-a195083918.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3665/syndey-a229414889.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3399/frankfurt-a359037364.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3361/kassel-wilhelmshoehe-a94680245.jpg)